Featured

Table of Contents

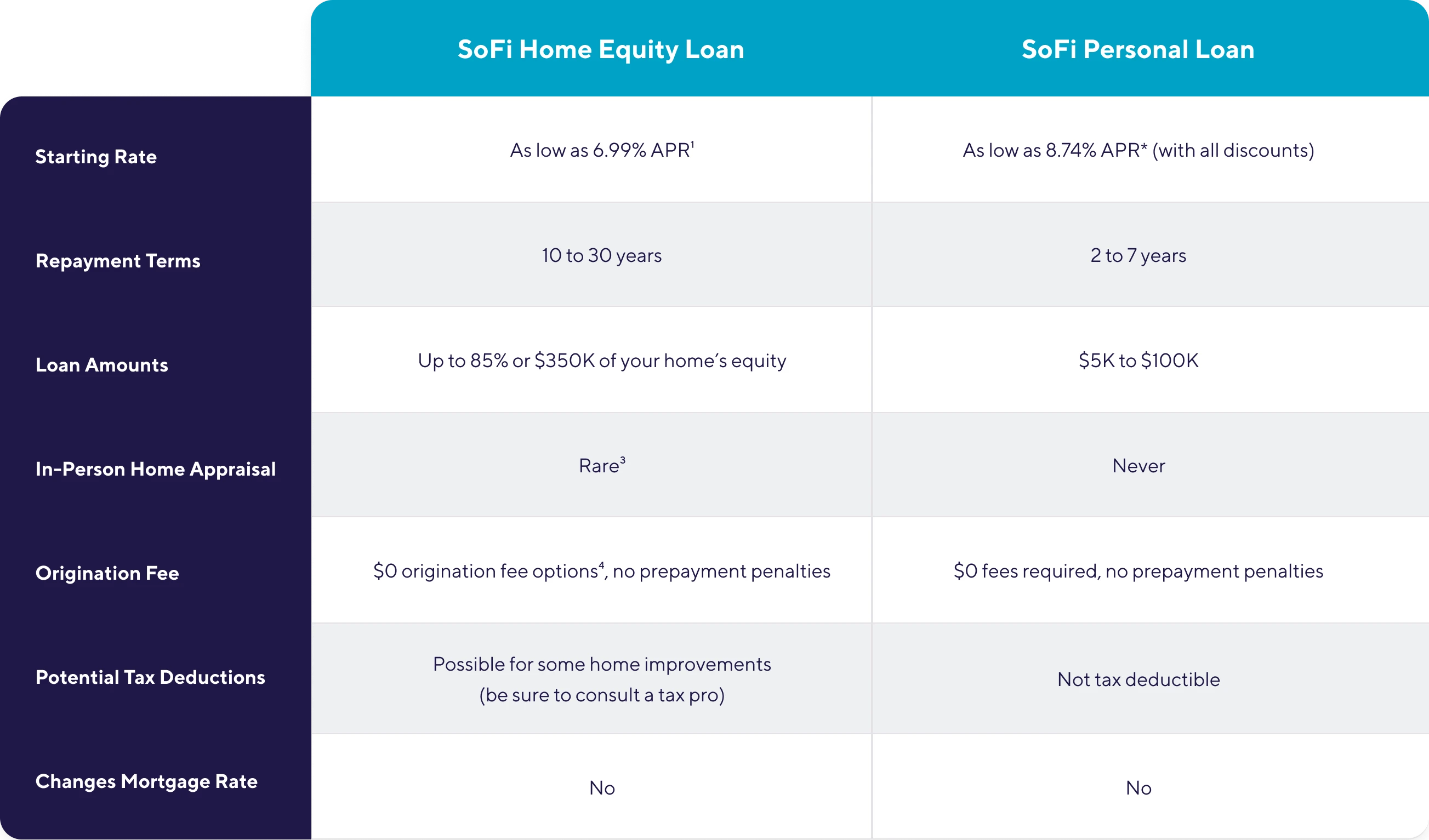

Tailor your loan with amounts from $3,000 to $100,000 and terms from 12 to 84 months.

When you register with Experian, you can view the loan uses that are matched to your credit profile. Some individuals call these "soft pull loans"; they are personalized loan deals matched to your credit profile that you are most likely to be approved for. Examining rates and your pre-qualified options generates a soft questions, which won't harm your credit rating if you aren't approved.

If you aren't at first approved, the application will stay as a soft query. Approval is not ensured with the initial application, as there may be extra verifications needed from the loan provider. If you are authorized for the offer, a difficult inquiry will be reported, in addition to the new account, which may affect your credit ratings.

Unbiased Analysis of Debt Management Programs in 2026

Registering or logging in to view the loan uses matched to your credit profile will not affect your credit history. When you use, selecting a loan labeled No Ding Decline will produce a soft questions if you aren't approved and won't affect your credit report. Typically, obtaining a loan, even if you aren't authorized, generates a difficult inquiry.

While that effect is normally very little and temporary, a single tough inquiry will generally take less than five points off your FICO Score, with this score effect staying for approximately a year. If you are authorized, a difficult query will appear on your credit report, along with the new loan account, which may impact your credit rating.

Your credit rating need to rebound within a couple of months, when you reveal your finances are steady with on-time payments. Eventually, your credit ratings may also enhance as your on-time payment history continues with accountable management of your new debt.

Exploring the Top Consolidation Rates for Q3 2026Discover the very best Personal Loans U.S.A. 2026. Compare leading loan providers, APR rates, approval suggestions, costs, and professional strategies to obtain safely with low interest and wise repayment. In 2026, individual loans will end up being one of the most versatile monetary tools for Americans handling rising expenses, debt combination, emergency situations, and large life purchases.

Navigating Debt-Relief Paths for 2026

Whether you are planning a huge purchase, managing financial obligation, or covering unanticipated costs, choosing the best personal loan in the USA can considerably affect your financial health. However, with hundreds of loan providers, different APR ranges, and concealed charges, selecting the best loan requires cautious understanding. This total guide will assist beginners, borrowers, and financing readers comprehend how individual loans operate in 2026 and how to discover the best low-interest alternatives safely.

Unlike home loans or automobile loans, individual loans usually do not need security. Key functions of personal loans: Fixed rates of interest (for the most part) Repaired monthly payments Versatile usage (financial obligation, medical, travel, and so on) Loan terms generally between 1 to 7 years Many loan providers in the USA offer individual loans varying from about $1,000 to $50,000, though some institutions offer loans approximately $100,000 depending on eligibility.

Comprehending interest rates is the primary step before making an application for any loan. In 2026, personal loan APRs differ substantially based on credit rating, income, and lending institution policies. Current monetary information shows: Typical individual loan rate around for customers with excellent credit Market APR variety approximately depending upon creditworthiness Top loan providers in early 2026 are offering competitive starting APRs such as: Around 6.49% (LightStream) Around 6.74% (significant banks) Around 6.99% (premium loan providers) However, single-digit APRs are usually reserved for borrowers with outstanding credit and strong financial profiles.

Numerous borrowers choose installment loans since they offer clarity and control over payment. Here are the main reasons Americans are selecting individual loans in 2026: Personal loans frequently have significantly lower rate of interest than charge card, making them perfect for debt combination. Unlike revolving credit, individual loans have actually repaired EMIs (monthly payments), which assists in budgeting and monetary preparation.

Many online lending institutions in the USA now authorize loans within 2448 hours, which is essential for emergency situations. Not all personal loans are the exact same. Understanding various loan categories helps you choose the very best choice based upon your financial goal. These loans are used to integrate numerous debts into one monthly payment, typically at a lower interest rate.

Critical Advice to Reducing Monthly Rates Through Consolidation

Online lenders typically supply much faster funding for emergency situation loans. These loans are offered for borrowers with low credit scores, though interest rates are generally higher.

This stability makes them much easier to manage compared to variable-rate credit alternatives. SoFi is one of the most recognized digital lending institutions offering competitive APRs, flexible loan terms, and no hidden fees for certified debtors. Why debtors select SoFi: Loan amounts up to $100,000 Fixed rates Unemployment security alternatives LightStream regularly ranks amongst top loan providers for borrowers with outstanding credit and offers some of the most affordable starting APRs in the market.

Common features: Moderate APR range credit union reliability flexible repayment choices Upstart uses AI-based underwriting models and thinks about factors beyond simply credit rating, making it a strong option for more youthful customers and those with limited credit report. Significant banks still offer competitive individual loan products with APRs beginning around the mid-single digits for certified candidates.

Best Paths for Clearing Off Debt for 2026

Typical rate expectations: Exceptional credit (750+): Least Expensive APR (610%) Excellent credit (690749 ): Moderate APR (1015%) Fair credit (630689 ): Greater APR (1525%) Poor credit (

{kind=link}

Latest Posts

Handling Multiple Credit Costs Through Strategic Planning

Utilizing Online Loan Tools to Plan Finances

Improving Money Management Knowledge in 2026